LP questions have moved past "who's your admin?"

If you raised a fund ten years ago, most LP diligence on operations sounded like:

- Who is your fund administrator?

- Who does your audit and tax?

- Do you have basic policies and controls?

That era is over.

Industry coverage shows LPs now digging deeply into how GPs run their back office and how they oversee third-party administrators, not just which names are on the pitch deck.

ILPA's DDQ, updated ODD guidance, and a growing ecosystem of LP-focused training make it easier than ever for investors to run detailed operational due diligence (ODD) processes.

If you are not prepared, the "ops section" of an LP meeting can quietly sink a fundraising process.

What LPs are actually trying to learn

While every LP has their own flavor, most modern ODD programs converge on five themes.

1. Governance and decision-making

LPs want to know:

- Who is responsible for critical decisions in finance, operations, and valuations.

- How conflicts are identified and managed.

- Whether there is meaningful segregation between deal teams and those who control books and records.

They are looking for signs that the firm is more than "a spreadsheet on a laptop."

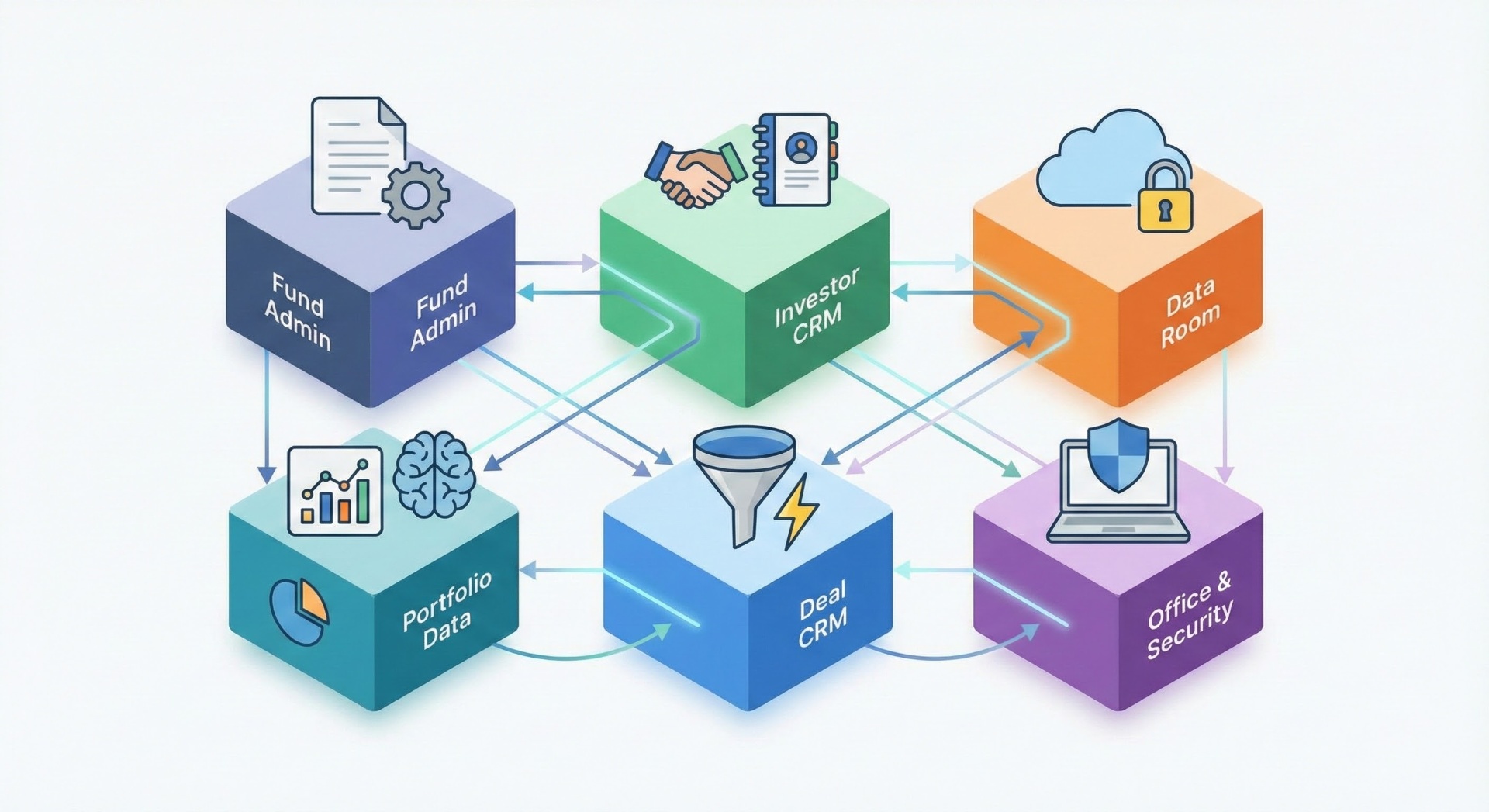

2. Data integrity and systems

Key questions include:

- What systems do you use for fund accounting, portfolio monitoring, and investor reporting?

- How do you ensure that data in those systems is complete, accurate, and timely?

- How do you reconcile administrator records, internal records, and bank statements?

Emerging best practice is to have a clear data model and controlled workflows rather than relying on ad hoc spreadsheets.

3. Valuation and reporting controls

LPs will ask:

- How are valuations determined and documented?

- Who sits on the valuation committee, and what is the process?

- How do you ensure that what is reported to LPs matches your internal records and governing documents?

If you are using AI or external valuation specialists, expect follow-up questions on oversight and methodology.

4. Service provider oversight

Using third-party administrators, custodians, and other providers is not a free pass. LPs want to see:

- Formal vendor selection and review processes.

- Documented SLAs and KPIs.

- Evidence that you monitor and challenge service providers rather than simply accepting whatever they send.

Recent commentary notes that LPs increasingly view weak oversight of service providers as an ODD red flag.

5. Operational resilience and cyber

Finally, LPs are looking at:

- Business continuity and disaster recovery plans.

- Cybersecurity posture, especially around investor data and sensitive documents.

- How you handle incidents, from data breaches to valuation errors.

"Auditor said we're fine" is not an adequate answer here.

How LPs structure ODD – and where managers stumble

Most institutional LPs use a combination of:

- Standardized questionnaires (often based on ILPA's DDQ 2.0 or their own variants).

- Document reviews (policies, org charts, sample reports, SOC reports).

- On-site or virtual meetings with finance, operations, compliance, and sometimes IT leaders.

Common failure points on the GP side:

- Inconsistent answers between the PPM, LP meetings, and ODD materials.

- Inability to demonstrate how a process actually works in the system (for example, how a capital call flows from approval to investor notice to cash reconciliation).

- Over-reliance on one person ("if Alex gets hit by a bus, we're in trouble").

None of these are fatal individually. Together, they create a picture of fragility.

Designing your back office to be "diligence-ready by default"

Instead of treating ODD as a once-per-fund event, use it as a design target for your operating model.

1. Map your critical workflows

At minimum:

- Capital calls and distributions

- Quarterly and annual reporting

- Valuations

- Fee and expense allocations

- KYC/AML and investor onboarding

For each workflow, document:

- Systems involved

- Roles and responsibilities

- Controls and approvals

- Evidence generated (logs, reports, reconciliations)

If you cannot draw the diagram, you cannot explain it under pressure.

2. Put your data on rails

LPs do not expect you to be perfect. They do expect:

- One system of record for fund accounting and investor balances.

- A clean portfolio data layer that ties documents, metrics, and valuations together.

- Reasonable reconciliation between internal and admin records.

This is exactly where an AI-enabled portfolio platform can help: automating document ingestion, structuring portfolio data, and giving you defensible audit trails instead of ad hoc spreadsheets.

3. Upgrade documentation from "we have a policy" to "we follow it"

Policies alone do not impress LPs. What does:

- Evidence that policies are actually followed – for example, signed valuation committee minutes, completed checklists, exception logs.

- A history of periodic policy reviews and updates as regulations and the firm evolve.

- Clear alignment between written disclosures, LPAs, and operational practice.

If something in your DDQ answer differs from reality, fix the process or the answer – not the story.

4. Get in front of known weaknesses

Most emerging and mid-market managers have operational gaps. LPs know this. What they react badly to is denial.

Better:

- Acknowledge where you are still building (for example, evolving tech stack, maturing cyber program).

- Show a concrete plan and timeline to address gaps.

- Demonstrate early progress (for example, recent system implementation, new hire, or third-party review).

This signals seriousness, not weakness.

A GP-side checklist before your next ODD

Before your next fundraising cycle or major LP meeting, work through a short internal checklist:

- ODD narrative: Can you articulate, in 5–7 minutes, how your back office works and why it is institutional-grade for your size?

- Evidence pack: Do you have a curated set of documents ready – org charts, policies, sample reports, SOC letters, admin agreements, valuation committee minutes, business continuity plans?

- System demo: Could your ops or finance lead screen-share the actual systems to show how a capital call, valuation, or LP report flows end-to-end?

- Service provider story: Do you have a crisp explanation of why you chose your admin and other vendors, how you oversee them, and how you would handle a change?

- Issue log: Do you have a record of operational issues (for example, late reports, errors, incidents) and how you resolved them?

If the answer to any of these is "not really," ODD will feel like an interrogation. If the answer is "yes," it becomes an opportunity to demonstrate that you are already operating at the standard LPs want.

Turning ODD into a competitive advantage

In a crowded fundraising environment, strong operations are not just a hygiene factor. They can differentiate you.

Managers who can confidently walk LPs through a clean, well-governed back office:

- Reduce time spent on follow-up questions and remediation.

- Build trust that carries over into future funds and co-invests.

- Have an easier time layering new products (continuation vehicles, SMAs, evergreen funds) on top of an existing platform.

ODD is not going away. You might as well design your operations so that you look your best under that microscope.

Want to see how GoodStream helps funds build diligence-ready operations? Book a demo and we will walk you through what "institutional-grade" looks like for your size.